Accrued expenses are costs that have been incurred but not yet paid for by the business. These are expenses that are recognized in the financial statements before the actual payment is made. The journal entry for an accrued expense typically involves increasing the expense account and recognizing a liability.

Accrued Expenses Journal Entry

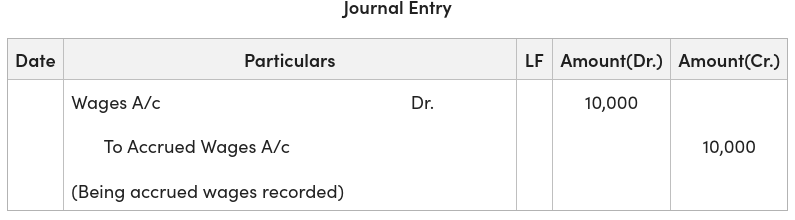

Journal Entry:

Examples of Journal Entries for Accrued Expenses

Example 1: Wages of ₹10,000 were accrued in the month of December. Record the necessary journal entry.

Example 2: Rent paid ₹50,000 for ten months, but the rent of two months, i.e., ₹10,000, remains accrued. Record the necessary journal entry.

Example 3: The electricity bill of ₹4,500 for March is unpaid at the end of the accounting period. Record the necessary journal entry.

Example 4: Interest of ₹6,000 on a bank loan is due but not yet paid. Record the necessary journal entry.

Example 5: Salary amounting to ₹20,000 for the last week of March is unpaid. Record the necessary journal entry.